If you are starting to think about your child’s financial future, you could open a Junior ISA (JISA) in their name or an Adult ISA in your name. Both offer valuable opportunities for savings and investments.

However, understanding the similarities and differences between these two types of ISAs is crucial for making the best decision for you and your child’s financial future.

This article will explore the important similarities and differences between Junior ISAs and Adult ISAs.

How are Junior ISAs and Adult ISAs Different?

There are a few key differences between Junior ISAs and adult ISAs that it’s important to highlight. These include:

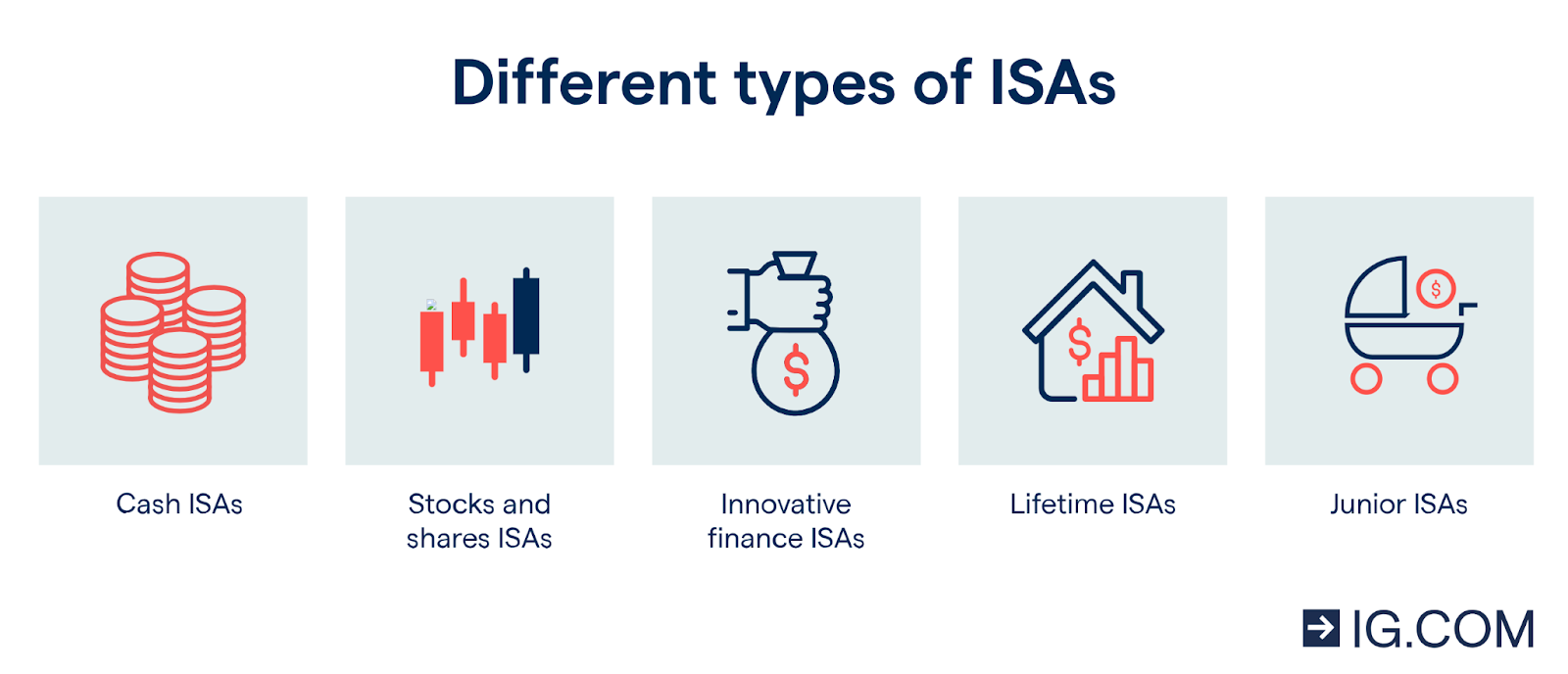

Adults Have More ISA Types Available

While you can only open a Junior Cash ISA or Junior Stocks and Shares ISA on behalf of your child, adults have a wider range of options when choosing a type of ISA. The ISA types for adults include:

- Lifetime ISA: Lifetime ISAs are used to buy your first home or save for later life. You must open a Lifetime ISA between 18 and 40, but you can put in up to £4,000 each year until you’re 50.

- Cash ISA: Cash ISAs are essentially just savings accounts that you don’t pay tax on.

- Stocks and Shares ISA: Stocks and Shares ISAs give you the opportunity to invest in funds, bonds, trusts, and shares.

- Innovative Finance ISA: Innovative Finance ISAs contain peer-to-peer loans. Peer-to-peer lending matches investors with borrowers, who could be individuals, businesses, or property developers. You tend to earn higher interest rates than other ISAs because you’re cutting out a bank.

(Image Source: IG)

Junior ISAs Have a Lower Annual Allowance

Every tax year – which runs from April 6th to April 5th – you can save up to £20,000 in one ISA account or split the allowance across multiple accounts. However, you can only pay a maximum of £4,000 into one Lifetime ISA each tax year.

Meanwhile, Junior ISAs have an annual allowance of just £9,000 per tax year across one or both accounts.

The annual allowance for both Junior ISAs and Adult ISAs does not carry forward into the next tax year.

You can Access The Money in an Adult ISA at anytime

You can take money out of an Adult ISA at any time without losing any tax benefits, which can be beneficial in providing liquidity for emergencies or significant life expenses. However, there may be charges for making withdrawals.

Meanwhile, if you consider a Junior ISA, the savings and returns can only be accessed once the child reaches the age of 18. This ensures that the money cannot be spent too early and offers a disciplined approach to saving.

Lifetime ISAs Receive Government Tax Relief

If you open a Lifetime ISA in your name to save for your child’s future, you will receive a 25% top-up from the government, up to a maximum of £1,000 per year. This is called tax relief.

Junior ISAs, on the other hand, are not given any money from the government.

How are Junior ISAs and Adult ISAs Similar?

Despite their differences, Junior ISAs and adult ISAs share some key similarities. These include:

They are Both Transferable

Adults can transfer all or part of their ISA savings from one provider to another anytime. It can be to a different type of ISA or the same type.

You can also transfer a Junior ISA to another provider at any time. In addition, if your child has a Junior ISA, it will mature into an Adult ISA when they turn 18. After this, it is still possible to transfer their ISA to another type of Adult ISA, such as Lifetime ISA, Stocks and Shares ISA, or Innovative Finance ISA.

To transfer your ISA from one provider or type to another, contact the ISA provider you want to move to and fill out their transfer form.

It’s important to note that children can only have one Junior Cash ISA and one Stocks and Shares ISA in their name, whilst adults can only have one Lifetime ISA, but there is no limit on the number of accounts with other ISA types.

They Both Offer Tax Advantages

Both Junior ISAs and Adult ISAs offer tax-free growth, meaning you won’t pay Income Tax on the interest or dividends or Capital Gains Tax on any profits from your investments.

These tax advantages make both Junior ISAs and Adult ISAs an efficient way to save and invest money.

Ready to Choose The Best Option for Your Child?

Junior ISAs are clearly focused on children, and they can only access the money once the account matures into an Adult ISA when they turn 18. However, if you prefer the flexibility and broader range of options for Adult ISAs, then you can open an account for your child in your name.