A business loan can be beneficial to business owners who need to make a large purchase or grow their business in some way.

However, you will be required to repay your business loan with added interest. So, knowing what you are getting into before applying for a business loan is essential.

This article will explore three things to do before you get a business loan.

Choose A Loan Type

The type of business loan you will apply for depends on how much money you need to borrow, who you want to borrow it from, and whether or not you can offer the lender some collateral.

There are a number of different types of secured and unsecured business loans to suit your business, including:

- Bank Loan. A bank loan is acquired from a bank, building society, or credit union and can be secured or unsecured. For secured loans, you will give the lender some collateral in the form of assets, which may be lost if repayments are not made.

- Mezzanine Finance. Mezzanine finance allows a business to borrow without putting up collateral. However, this means the lender can claim part-ownership of the business if the money is not paid back on time and in full.

- Asset-Based Finance. Asset-based finance allows you to borrow money using a business asset as collateral. The lender will prioritize the quality of the asset over the business’s credit score or prospects.

- Microloans. Microloans are smaller loans of $100,000 or less. Banks are less likely to give out these loans than alternative lenders. When they do, the decision is based on your business’ credit score.

When choosing a loan type, it’s important to compare all the related fees. This may include underwriting fees, administration fees, loan processing fees, establishment or application fees, exit fees, early repayment fees, valuation fees (if you choose to secure your loan), and ongoing monthly fees.

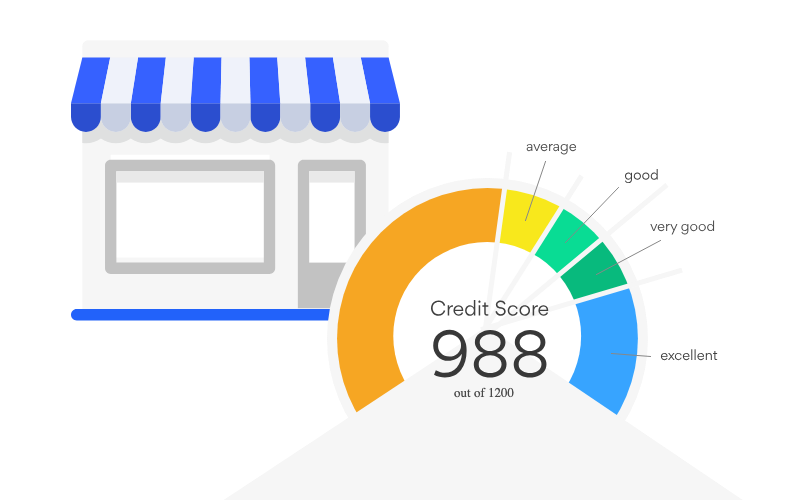

Improve Your Credit Score

A business credit score is a numeric value between 0-1200 that reflects a company’s financial health and reliability. The score is obtained from your business credit profile, which contains information about your business’s credit history.

The minimum credit score needed to acquire a business loan will vary depending on the type, amount, lender, and other terms. Generally, a higher credit score – anything above 680 – will increase your chances of approval and give you access to better terms.

(Image Source: Lend)

The lender you approach will ask to see proof of your credit score and other business documents related to your finances.

Here are some ways to improve the credit score of your business:

- Update your profile with all the credit bureaus. Equifax, TransUnion, and Experian are the three main credit bureaus that collect your information and create your score. Updating your credit profile with all three bureaus is essential, as they have slightly different formulas for creating business credit scores.

- Pay your bills on time. One of the easiest ways to improve your credit score is to ensure you pay all your bills on time, including those to lenders, vendors, utility companies, and landlords. Payment trends such as mobile wallets, automatic bill payments, and online banking have made it easier for businesses to stay on top of their bills.

- Open another business credit card account. Getting another business credit card can improve your credit score, as it proves to lenders that you can manage different types of credit. Just make sure you stay on top of your spending and monthly payments.

Securing a business loan with a bad credit score can be challenging, as lenders will instead scrutinize other aspects of your business, such as cash flow, revenue, and the length of time you’ve been in business. In addition, you will also be required to provide collateral or a personal guarantee.

Calculate What You Can Afford To Repay

Finally, you need to calculate what your business can afford to repay each month after you have taken the loan. You can do this by reviewing your past financials and completing cash flow forecasts.

Your monthly loan repayment amounts will vary depending on the loan amount and length of time. Your lender will outline the repayment terms before you sign for the loan, but it is a good idea to have a monthly figure in mind before you get to this stage.

Ready To Apply For a Business Loan?

If you are ready to apply for a business loan, then make sure to follow the three steps above.

Firstly, you need to know which type of loan you want to apply for and what credit score you need to do so; then, you can put measures in place to boost your credit score if it doesn’t yet meet the requirements.

Finally, you can figure out how much you can afford to repay each month so you can go to a lender with this figure and avoid hidden costs.